Source/Contribution by : NJ Publications

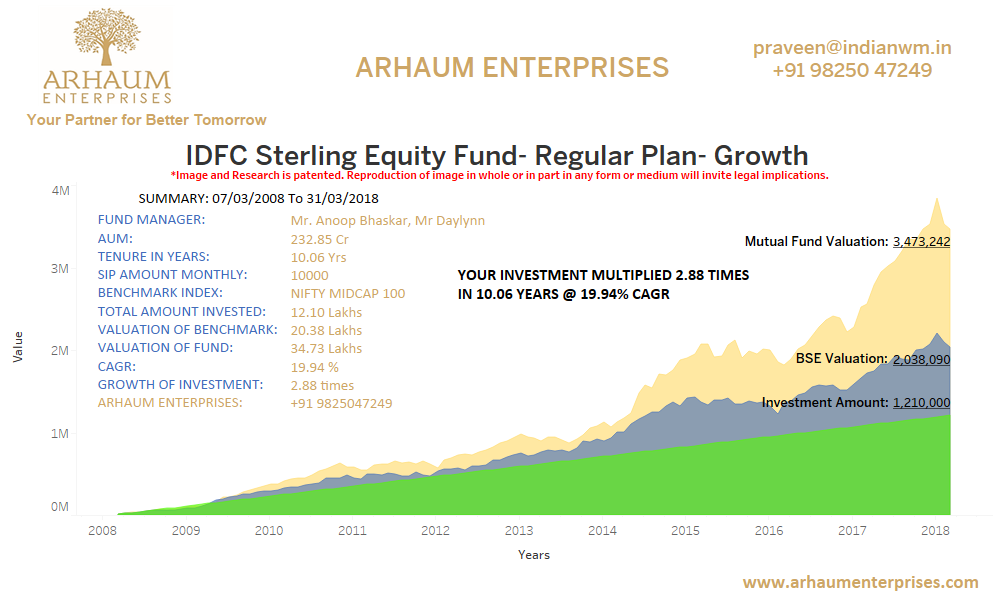

Another year full of surprises and shocks, has formally come to an end. Although, the introduction of GST did create ripples, businesses were hit for some time, but we are on a recovery mode. 2017 was one of the best years for Indian Equity Markets since the 2008 global recession. The markets were on a roll, with the major indices delivering more than 25% return for this year, the mutual funds industry witnessed equity inflows of Rs 178,878 Cr in the year 2017. Things are going great. Certainly, investors have made money during the year, and now it’s time to start gearing up for the next year. At this point, we have penned down a list of steps, some do’s and dont’s which can help you get the maximum out of the year 2018 and onwards financially.

Don’t Redeem your long term investments for the markets are trading high: Your long term investments should not be left at the mercy of the 2008 recession or the 2017 boom. Many market gurus are propagating that this is the “market peak” and it’s the “right time” to liquidate your investments. Well, we don’t know whether this is the peak, and we are sure neither do they. The markets are forever subject to volatility, they might correct or they might surge. Our long term goals cannot be achieved if we start timing the volatile markets. If you liquidate the investment kept for your daughter’s wedding, which was up 50% from the time you invested, hoping to re-invest when the markets correct. What if the markets do not correct any soon, or even if they do, how would you know when they are at their lowest, what if the money you redeemed vanishes while meeting your current liquidity needs. Although, your 10 lacs did come back to you as 15 lakhs, but your daughter’s wedding goes for a toss.

Don’t stop your SIP’s: On the same logic as above, it is not prudent to stop your SIP’s. The Rupee Cost Averaging will work to average out the cost of your investment whether this is the peak or whether Indian markets continue with the bull run. And your uninterrupted long term investments will ensure that you make the most of the Power of Compounding, while controlling the cost with Rupee Cost Averaging. The idea behind the SIP mode of investing is imparting discipline and peace of mind to the investor by saving him the stress caused by constantly checking as to what would be the right time to invest and redeem.

Stay away from:

- Gold: Gold one of the most trusted and sought after investment product is gradually losing its sheen, for the simple reason, people aren’t making money, it’s reflecting in the gold import volume also, which is consistently on the decline since 2011. Gold prices have remained flat over the past few years. And apparently, there are no signs of a quick turnaround in 2018, so avoid investing in Gold. Restrict gold purchase to the once in a while impulsive purchase of an exquisite jewelery piece only. Don’t buy gold hoping to get a return from it.

- Real Estate: Another favourite of Indian investors isn’t an attractive investment opportunity for this year also. Like gold, property prices have also remained stagnant for most parts of the country, in fact in some places, the prices have alleviated. Plus the RERA Act and the government restrictions imposed on real estate, as it was earlier a safe haven for parking black money has further smudged the sector. So, at this point in time, apart from the house you are acquiring for self use, limit your investment Portfolio’s exposure to Realty.

- Traditional Debt instruments: The interest rates are consistently falling, and it makes no sense to invest your hard earned money in a fixed deposit for a meagre 6-7% return. The after tax return may not be even able to cover the inflation cost. In fact, the government has announced the last cut on small savings rate (PPF, NSC and KVP) just a week back. So, stay away from FD’s and other low return yielding products, instead look at bonds, debt Mutual Funds if you want to keep your risk low, while generating better, tax efficient returns.

Review your home loan: When the deposit rates are falling, so are the loan interest rates. So, if you have an ongoing home loan, ensure you are being levied the new reduced rates. Meet your banker, and seek options for reducing the interest rates, like switching to the adjustable interest rate option, or switching to a lower interest rate plan, etc. Follow the Plan of Action and have a happy and a prosperous New Year!