India’s retirees are standing before a difficult choice. They can switch to equity funds, or they can head for old-age poverty. Am I being too dramatic when I say this? Perhaps. I know that some people do not like phrases like ‘old-age poverty’ because it’s a prospect that is too frightening to contemplate. However, that’s part of the reason I use it; it’s something that Indian retirees need to think about urgently, even if they have to be shocked into doing so.

Subscribe to the Value Research Insight newsletter

I’ve said this earlier too but the situation is now getting worse because of dropping interest rates. Because the NDA government is managing its fiscal deficit well, it is more than likely that the returns from deposits will keep heading downwards. The economy may be better off, but that is not much comfort for the retiree who is past his or her earning life. If you are dependent on a deposit for income, then you are heading for large cuts in your income. A cut from 8.5 per cent to 7.5 per cent in a deposit rate means that you lose almost 12 per cent of your income. If interest rates keep dropping, it could get much uglier.

Clearly, the general advice about sticking to fixed-income deposits of various kinds because they are the only safe option for retirees, since equity is too risky, is wrong. It’s not just wrong, but it’s utterly misguided and any senior citizen following it will head for financial disaster.

Unless you have an inherently inflation-adjusted source of income like rent, at some point you are going to face this problem. Interest on deposits will not keep up with inflation and the money you’ll withdraw for your expenses will relentlessly eat into the real value of your savings.

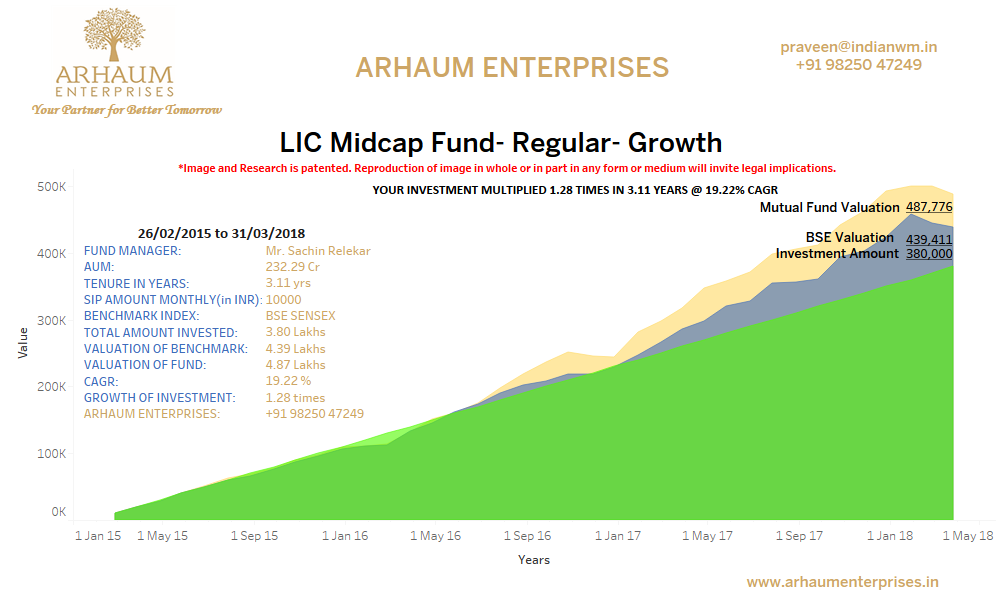

So what’s the solution? Clearly, retirees must invest in equity mutual funds. Looking backwards, let’s take a real example of equity investments. Suppose you had retired in early 1980 with a kitty of R5 lakh that you had invested in a hypothetical investment that tracked the Sensex. Let’s say that your monthly expenses were R3,000 a month and grew at 10 per cent a year.

After 32 years, your monthly expenses would be R63,000. Not only would you have no trouble funding these expenses, your principal would have grown to R2.7 crore! What about the risk? During these years, the investment would have faced up to steep declines in 1987, 1992, 2001 and 2008 and taken them in its stride comfortably. The lesson is clear: if retirees want to spend their twilight years prosperously, then equity is their only hope.

However, I understand that the real barrier is psychological. The fact that equity is risky and fixed income is safe is deeply embedded in our minds, especially in the generation that is now retired or is retiring. So what can be done about this? My firmly held belief is that this problem is not financial, and there are no financial solutions. It’s a problem of mindset and must be cured by changing mindsets.

Over short periods of time, equity is volatile. At the same time, over long periods of time, it is not risky. On the other hand, if you take the real value into account (after considering rising prices), then deposits are not just risky, they are certain to be disastrous.

This is not easy to accept, but it’s the only way.